The S&P 500 (+1.4% in USD YTD) has shown clear signs of exhaustion since the beginning of the year. Even Nvidia’s (still) very strong results are no longer enough to sustain momentum, largely due to the emergence of DeepSeek, which challenges U.S. dominance in AI. The so-called “Magnificent 7” have stalled in performance, with their index undergoing a significant correction (-12% from the December peak). Donald Trump’s agitation also seems to be turning against the U.S. in the short term, increasing uncertainty—especially regarding the impact of the DOGE cost-cutting program on employment and the effect of tariffs on inflation. Over the past few weeks, consumer confidence has sharply declined, as have long-term U.S. interest rates (-0.4% for the month).

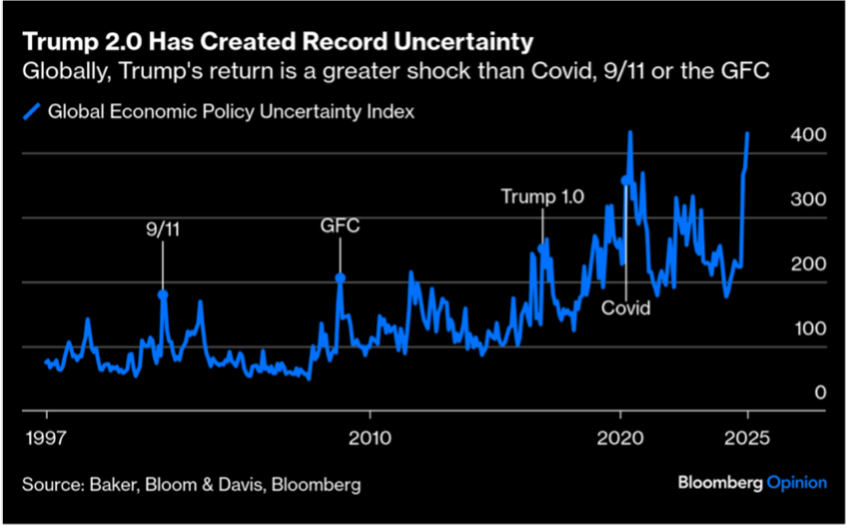

Trump’s election: so far, its impact has been a significant rise in uncertainty.

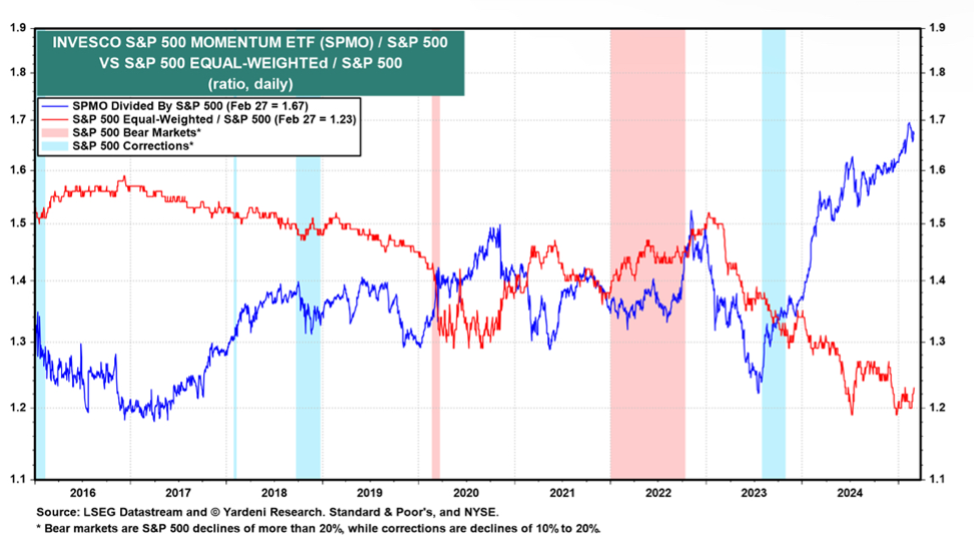

Conversely, Europe (+10%) and China (+14%) have been the biggest beneficiaries of this market shift. At the start of the year, capital flows have moved in the opposite direction, with institutional investors seemingly rediscovering the Old Continent. The rebound in European indices has so far been driven by an increase in valuation multiples (from 13.5x to 14.5x), rather than by better-than-expected Q4 earnings. Our scenario of a trend reversal—where the overvaluation and excessive overweighting of the U.S. market compared to other markets and investment styles—has begun to materialize, though there is still a long way to go, given the extreme outperformance of growth and momentum investing (compared to value investing) since autumn 2023.

Factor analysis of the S&P 500: Outperformance of the momentum factor relative to the S&P 500 (blue) and underperformance of the equal-weighted S&P 500 versus the S&P 500 (red).

To the disbelief of many Europeans, the new Trump administration can at least be credited with making its intentions clear. In a document that went relatively unnoticed upon its release, the new White House economic advisor outlines the administration’s goal to deeply reform the global monetary system¹. In this strategy, tariffs are seen as a key tool to rebalance the U.S. trade deficit and strengthen domestic industry against foreign competition, particularly from China. According to the administration, this can only be achieved by correcting the persistent overvaluation of the dollar and, if necessary, linking national security to trade policies.

Major U.S. trade partners would, in one way or another, be forced to contribute to the cost of their protection—or risk losing it entirely in the case of non-compliance and/or facing exorbitant tariffs. This approach could even extend to mandatory participation in the restructuring of U.S. debt to avoid a solvency crisis for Uncle Sam. Such a move would support both lower long-term interest rates and a weaker dollar.

For now, these rumors should at least sustain demand from emerging-market central banks seeking to reduce their dollar reserves. In this environment, gold unsurprisingly reached a new record high of $2,943/oz in February.

For the rest of the year, the U.S. market will continue to set the tone for global finance. We believe caution is still warranted. The current tariff situation could result in a temporary inflation spike and a short-lived slowdown—or, conversely, escalate into major trade tensions leading to a significant economic downturn. At this point, no one can say for certain. However, the valuation of the S&P 500 remains extremely high, representing a risk in itself. It may seem incredible, but if valued at its historical average, the S&P 500 would be around 4,500 points instead of 6,000. Caution is advised in case the current valuation premium suddenly disappears.

¹ « A User’s Guide to Restructuring the Global Trading System », Stephen Miran, Nov. 2024

Article written by Bertrand Veraghaenne

Over 25 years' expertise in financial markets

Bertrand Veraghaenne has over 25 years' experience in the financial markets. He started at Arthur Andersen in 1997, joined Petercam in 2000 as a financial analyst, then headed the financial analysis department of Petercam Asset Management in 2005, contributing in particular to the creation of an emerging fund.

In 2009, he became head of the financial analysis department at BNPP-TEB in Istanbul, before joining Private Banking in 2010 as Chief Economist of Banque Transatlantique (CIC-Crédit Mutuel), working between Brussels and Paris. In 2013, he joined JPMorgan Private Bank, holding key positions in London and Luxembourg as Investment Specialist for UHNWI clients in Benelux and Denmark.

In September 2024, he joined Whitestone Partners, a Whitestone Group company, to look after the ARMS multi-asset fund, which is a Luxembourg Specialised Investment Fund. From now on, he will regularly share his views on the market in our newsletter and blog.